Each year the Mergers & Acquisitions Committee of the American Bar Association prepares a detailed study entitled the Canadian Private Target M&A Deal Points Study. This study covers a sample of 101 publicly available acquisition agreements and covers transaction values of from less than five million to greater than half a billion dollars. This is a must-read study for M&A professionals. In this two part blog I will be summarizing what I believe are the highlights of the study. This is part one.

FINANCIAL PROVISIONS

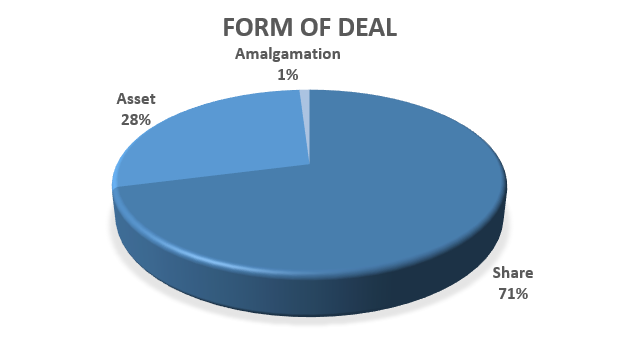

Form of Deal (share versus asset)

Share purchases constitute most the transactions with 71% of the transactions being the purchase and sale of shares. This preference has been consistent year over year in Canada.

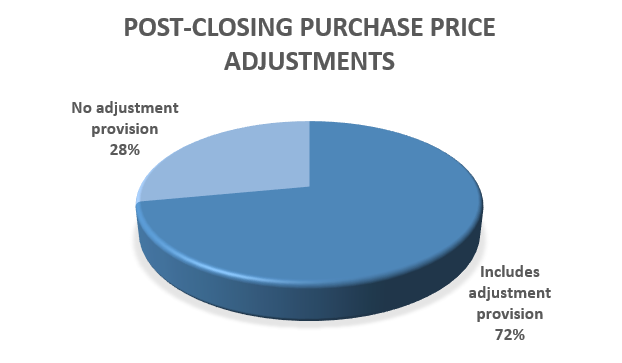

Post-Closing Purchase Price Adjustments

The study shows that post-closing purchase price adjustments are becoming increasingly common year over year. The most common metric used for the purposes of this adjustment is Working Capital which amounted to 83% of the adjustment metrics. In most cases the Purchaser was responsible for preparing the Closing Balance Sheet that was to be used for the purposes of the post-closing purchase price adjustment – 76% of the time (verus 52% in 2012). “GAAP” or “GAAP consistent with past practices” accounted for 62% of the preferred accounting methodologies.

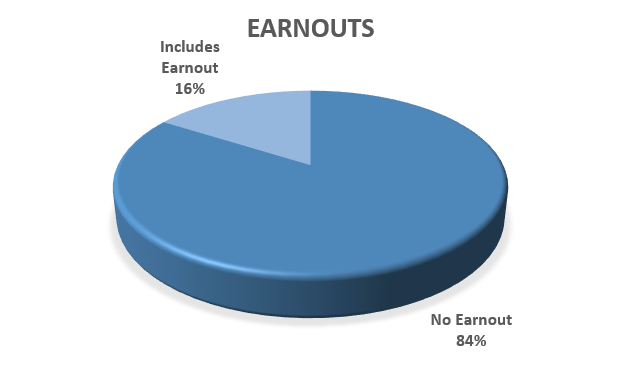

Earnouts

Unlike post-closing purchase price adjustments, the popularity of the use of earnouts appears to be on the decline year over year (showing a decline of 8% to the inclusion rate in 2014). “Revenue” and “Earnings or EBITDA” account for 63% of the preferred metrics used in determining the earnout target. Also of importance is the shift in the period of the earnout – for example, 33% of earnouts in 2014 were for a duration of 12 months versus 6% in 2016; 20% of earnouts in 2014 had a duration of 36 months versus 38% in 2016.

PERVASIVE QUALIFIERS

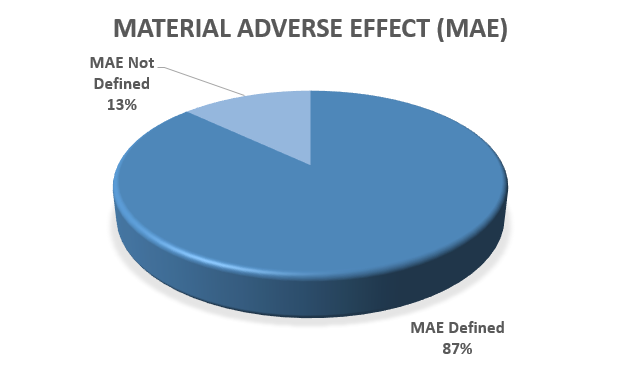

Definition of Material Adverse Effect

The study showed that the used of a definition for the term “Material Adverse Effect” in purchase agreements is growing in popularity with 87% of the agreements providing a definition for the term. This is likely as a result of the growing effort among M&A lawyers to draft more clear and unambiguous agreements. Another interesting fact is that 100% of the studied agreements included a material adverse effect clause which has not been traditionally the case.

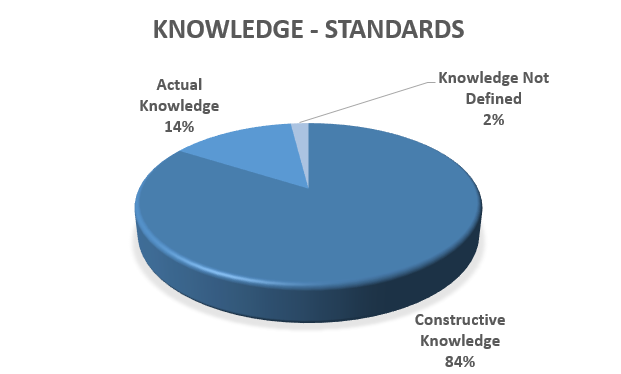

Knowledge

The definition of what constitutes “knowledge” of a seller or purchaser in an M&A purchase agreement has become more broadly drafted year over year. The inclusion of a definition of “knowledge” is used in 98% of the studied agreements versus only 83% in 2012. In addition, the breadth or scope of the definition of “knowledge” to include what constitutes “constructive knowledge” has increased substantially from 69% in 2012 to 83% in 2016. This is a sign that buyers are pushing for higher standards of “knowledge” and more accountability from the seller with respect to the company they are buying and the representations and warranties that are being given by the seller.

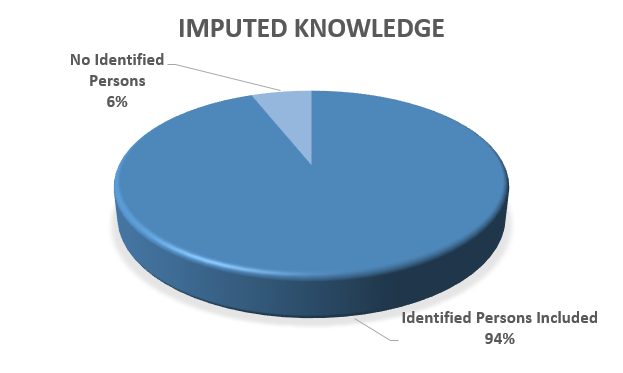

Identifying persons with imputed knowledge has also grown substantially from 78% in 2012 to 94% in 2016. This means that in 94% of the agreements at least one person (e.g. officer, director, principal shareholder) has been identified as a person whose knowledge is imputed into the definition of “Knowledge”, thus bolstering the integrity of the representations and warranties of the seller.

Part 2 of 3 will be coming shortly.